Help to Buy

Who is Eligible?

If you are a first-time buyer in England, you can apply for a Help to Buy: Equity Loan, which is a loan from the government that you put towards the cost of buying a newly built home with a price tag of up to £437,600 in the south east region.

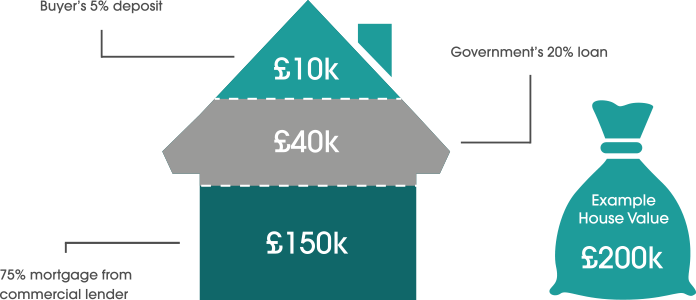

You can borrow a minimum of 5% and up to a maximum of 20% (40% in London) of the full purchase price of a new-build home. You must buy your home from a homebuilder registered for Help to Buy: Equity Loan.

The equity loan, the deposit you have saved, and your repayment mortgage cover the total cost of buying your newly built home. The percentage you borrow is based on the market value of your home when you buy it.

You do not pay interest on the equity loan for the first 5 years. You start to pay interest in year 6, on the equity loan amount you borrowed. The equity loan payments are interest only, so you do not reduce the amount you owe.

You can repay all or part of your equity loan at any time. A part payment must be at least 10% of what your home is worth at the time of repayment.

You won’t be able to sublet this home or enter a part exchange deal on your old home. You must not own any other property at the time you buy your new home with a Help to Buy: Equity Loan.

How Does It Work?

Example: for a home with a £200,000 price tag

If the home in the example above sold for £210,000, you would receive £168,000 (80% from your mortgage and the cash deposit) and you would pay back £42,000 of the loan (20%). You would need to pay off your mortgage with your share of the money.

Paying back the equity loan

When deciding if an equity loan is right for you, it’s important to consider the full cost of your borrowing:

For the first five 5 years:

- the equity loan is interest free

- you pay a £1 monthly management fee by Direct Debit.

From year 6:

- pay the £1 monthly management fee

- pay monthly interest fee of 1.75% of the equity loan

- interest rate will rise each April by the Consumer Price Index (CPI), plus 2%

- continue to pay interest until you repay your loan in full

When you take out your equity loan, you agree to repay it in full, plus interest and management fees.

You must repay your equity loan in full:

- at the end of the equity loan term

- when you pay off your repayment mortgage

- when you sell your home

- if you do not follow the terms set out in the equity loan contract and we ask you to repay the loan in full

The amount you pay back is worked out as a percentage of the market value at the time you choose to repay. If the market value of your home rises or falls, so does the amount you owe on your equity loan accordingly.

How To Apply?

The Help to Buy: Equity Loan scheme is run by Government-appointed Help to Buy agents. They can guide you through your purchase, from providing general information about the scheme to dealing with your application.

Or look out for the Help to Buy logo on new-build developments and ask about the scheme there.

Frequently Asked Questions

Can I buy a home off plan?

Yes. You are able to reserve a new home off plan at any time. However, you need to complete the sale within six months from the exchange of contracts. You also need to ensure that your mortgage offer is valid through to legal completion.

Can I buy with an interest-only main mortgage?

No. Your main lender’s mortgage must be a repayment loan with interest and capital repaid every month. This ensures you make the Help to Buy purchase on a sound basis and protects the tax payers’ investment in your home.

Can I part exchange my existing home for a Help to Buy home?

No. Part exchange is not available. House builders selling Help to Buy homes cannot offer a part exchange sale.

Will I have to pay Stamp Duty?

The Government’s standard rules and procedures for Stamp Duty Land Tax (SDLT) apply to all Help to Buy purchases.

SDLT is payable at the time of purchase, on the full purchase price of the home. That is, the amount paid by you (the first mortgage and any cash contribution) plus the value of the Help to Buy loan.

There is no further SDLT to pay on any ‘staircasing’ repayments or repayment when the home is sold.

You should budget for SDLT on the full open market price of the property when you purchase a Help to Buy home.

Who pays for repairs and ongoing maintenance to my home?

You will own 100% of the property, therefore,it is your responsibility to repair and maintain your home. New homes often come with a guarantee that will cover certain defects for up to 10 years after it was built. This guarantee usually only covers defects in the house builder’s workmanship. Your solicitor/conveyancer will be able to advise in more detail on this.

Who provides the Government's contribution for Help to Buy?

The equity loan is provided by the Homes and Communities Agency and administrated by your local Help to Buy agent. The contribution is secured by a second charge on your property title registered at the Land Registry.

How long will it take before I can move in?

Because Help to Buy: equity loan homes are generally on new developments (and may still be under construction), in common with most new home sales, you will normally be expected to arrange a mortgage and exchange contracts within one month of paying your reservation fee.

Your moving in date may depend on the time required to complete construction work – this will vary from scheme to scheme. Some Help to Buy applicants may need to wait for a longer period of time for a home that matches very specific needs whereas others may buy from a development that allows you to move in earlier.

What happens if the completion of my home is delayed?

Once you have committed to buying a home (at exchange of contracts) the house builder will have agreed to build the home and keep you informed of progress. If you are unhappy about any delays in construction you must speak to the house builder. Your solicitor/conveyancer will be able to advise on the house builder’s contractual responsibilities before you agree to the sale. You should check with your house builder that the funding will be available on the date you expect to complete your purchase.

Are there any restrictions on the properties that I can purchase?

All Help to Buy: equity loan homes are on new build developments where the Homes and Communities Agency has a registration agreement with the house builder. You can only purchase from these house builders. The maximum purchase price is £437,600 in the south east region.

Can I sublet my Help to Buy home?

No. Help to Buy is designed to assist you to move on to or up the housing ladder. If you wish to sublet, you will first have to repay the Help to Buy: Equity Loan assistance. In exceptional circumstances sub-letting may be considered. For example, if you’re a serving member of the Armed Forces staff whose tour of duty requires you to serve away from the area in which you live for a fixed period. In these circumstances you would also require approval from your mortgage lender.

Can I own other homes and buy a Help to Buy home?

No. Help to Buy is designed to assist you to move on to or up the housing ladder and must be your only residence. This means you will be expected to sell your current home if moving up the ladder. The disposal of your current home will be verified by your solicitor/conveyancer before you can proceed to exchange contracts on your Help to Buy home.

Can I own a Help to Buy home and buy a second home?

No. If you can afford to purchase another home you will have to repay the Help to Buy: Equity Loan.

The property purchased must be your only residence. Help to Buy is not available to assist buy-to-let investors or those who will own any property other than their Help to Buy property after completing their purchase.

You cannot rent out your existing home and buy a second home through Help to Buy.

Applicants who make fraudulent claims for Help to Buy assistance will be liable to criminal prosecution. Fraudulent claims will always require immediate repayment of the equity loan.

Can I use cash from my council, Housing Association or other public sector body to buy with the addition of help through Help to Buy?

Yes, provided that your local council is satisfied that this represents value-for-money and the other funding is compatible with Help to Buy. Any funding provided that must be secured against your home would not be compatible with the Help to Buy scheme.

After purchasing my home, can I increase my mortgage or take out another loan?

Not without permission from the Post Sales Help to Buy Agent. Further advances must be approved by the Post Sales Help to Buy Agent.

Advances to be used for repaying the equity loans in part (staircasing) or full will usually be welcomed and approved. Advances for other purposes will be considered by the Post Sales Help to Buy Agent on a case by case basis (see question below regarding extending or altering the property).

You may be able to transfer your mortgage to another lender taking part in the scheme following scheme following prior permission from the Post Sales Help to Buy Agent. However, you must ensure your new lender is informed that your home is a Help to Buy property with a second charge entitling the Homes and Communities Agency to a share of the future sale proceeds. You should note that not all lenders will accept a remortgage where there is already an equity loan in place.

The Post Sales Help to Buy Agent may decline permission for further advances or transfer to another lender if after assessment they consider you may be putting yourself in an unsustainable financial position.

Can I extend or alter the property?

Not without permission. Because Help to Buy is designed to help people move on to or up the housing ladder, you should consider repaying part or all of the Homes and Communities Agency’s contribution before making plans for improvements or alterations. This is because the Agency is seeking to help future aspiring buyers and may use the proceeds of these repayments to make more assistance available. Therefore, consent will not usually be granted for significant home improvements. The Post Sales Help to Buy Agent will act reasonably in considering any application and will review cases of hardship if, for example, property modifications are required for a disability.

When your property is sold in the future, if improvements have been made with the approval of the Post Sales Help to Buy Agent, these will be ignored when your property is valued to work out how much should be repaid to the Agency.

After five years of ownership how is the fee collected?

Fees can be paid in a single yearly payment or in monthly instalments.

The Post Sales Help to Buy Agent will collect your fee by direct debit or standing order. They will contact you at least a month before your fees are due, to set up your repayment arrangement. If you do not pay by Direct Debit, you will pay an additional administration charge (currently £4 per month).

You will also receive a statement each year confirming when your fees are payable. The annual statement will also show any payments you have made once you start paying the fee.

What if I die after purchasing a Help to Buy home?

This depends on whether you bought your home alone or with others.

If you bought the house/flat on your own and you die, the home will be passed on in the normal way under the terms of your will and the payments explained in this guide will be made by your estate in accordance with the scheme. If you have not made a will it will pass under the laws of intestacy.

It is recommended that a sole buyer seeks independent legal advice about this.

If you bought your home with others and one of them dies, their interest in the property will either be transferred to the surviving co-owner (s) or will pass under the terms of their will, or (if there is no will) the laws of intestacy.

It is recommended that where there are two or more owners, they seek independent legal advice about this.

Can I get help with benefits to pay the Help to Buy fees if, for example, I lose my job?

Because Help to Buy fees are not classified as rent, they do not qualify for Housing Benefit. You should make sure you have made arrangements to ensure you can continue to make your Help to Buy payments if your income stops. You should seek independent financial advice about this before purchasing a Help to Buy home.

What happens if my partner moves out and no longer wants to be party to the equity loan agreement?

The Post Sales Help to Buy Agent will be able to arrange for a ‘Deed of Release’ which will release your partner from the obligation of having to repay the equity loan. Assuming that your first charge mortgage lender is content for this to take place and that you are able to provide evidence that you can meet your housing costs and still have a reasonable standard of living, permission should be a formality.